Measuring What Matters: Inside the Evolution of Institutional Dark Pool Innovation

Measuring What Matters: Inside the Evolution of Institutional Dark Pool Innovation

How Infrastructure Providers and Technology Platforms Are Enabling Genuine Venue Innovation By Enrico Cacciatore October 2025

This research was originally published in TabbFORUM, the leading voice in capital markets technology and institutional trading strategy.

Read on TabbFORUM →EXECUTIVE SUMMARY

Asset managers overseeing trillions in capital face an uncomfortable truth: they can't distinguish between the ATSs preserving their alpha and those simply fragmenting their flow. Current transparency infrastructure shows execution outcomes but hides routing decisions—measuring what filled while ignoring what didn't, where it went, and why. In this report, CalcGuard Technologies Chief Product and Strategy Officer Enrico Cacciatore examines how infrastructure providers and venue innovators are illuminating the complete order journey, making the $11 billion execution opportunity finally measurable.

Infrastructure Enablers

MEMX provides exchange-grade reliability through Market-as-a-Service (MaaS), enabling venues like Blue Ocean to achieve 100% uptime without capital-intensive buildout

Fidelity Service Bureau (FSB) delivers broker-neutral connectivity and venue-level performance attribution, democratizing execution measurement previously available only to the largest asset managers

Venue Innovators

IntelligentCross (16.1% market share) leads through ML-driven timing optimization, performing 66 million daily calibrations that neutralize adverse selection (trading against better-informed counterparties) without participant segmentation

PureStream (3.7%) matches orders on volume commitment (LTR), then streams proportional fills to both counterparties in real time as SIP reference trades print

Blue Ocean (2.1%) extends market hours with overnight trading across 5,000 securities, bridging U.S., Asian, and European price discovery

AlphaX US (1.8%) validates that batch auctions achieve institutional adoption through 10-millisecond collection windows and bilateral price improvement

Key Findings

This report establishes a four-tier taxonomy classifying all 33 ATSs by structural innovation:

Tier 1 (31.4% volume): Structural innovators using ML-driven timing, probabilistic matching, or temporal extension

Tier 2 (42.3% volume): Sophisticated segmentation with mark-out-based participant classification

Tier 3 (14.7% volume): Standard segmentation with basic tiering

Tier 4 (11.6% volume): Commodity midpoint matching with minimal differentiation

Market concentration is extreme: Top 5 venues capture 51.4% of market share, while the bottom 23 venues collectively handle less than IntelligentCross alone. This concentration reflects institutional flow responding to measurable differentiation when transparency infrastructure enables comparison.

Infrastructure concentration risk: Analysis of all 33 ATS-N filings reveals 69% of venues operate from adjacent NY4/NY5 data centers in Secaucus, NJ creating systemic resilience concerns that rational market economics inadvertently produced.

The 80-95% non-fill problem: Most routes to ATSs never execute, creating information leakage vectors that sophisticated participants exploit through systematic probing. Without complete routing transparency capturing every venue attempt, timestamp, and failed reason institutions cannot distinguish venues with poor efficiency from those with sophisticated adverse selection (trading against better-informed counterparties) protection.

Market consolidation is inevitable. Tier 3-4 venues handling <1% market share cannot justify regulatory compliance costs as transparency platforms enable empirical venue comparison. The future belongs to venues that can explain their trading, not just execute it.

The Path Forward

The market is moving toward greater transparency and measurement rigor. Asset managers increasingly prioritize venue-level attribution over aggregate placement performance, recognizing that execution quality requires separating broker routing decisions from venue mechanics. Leading institutions are conducting empirical A/B testing across venue tiers to identify measurable differentiation.

Broker-dealers face consolidation pressure as operational efficiency and regulatory overhead make redundant ATSs economically unsustainable. Transparency platforms enable clients to compare performance empirically, rewarding venues with genuine structural innovation while exposing commodity matching that adds complexity without execution improvement.

Regulators are examining opportunities to expand ATS-N disclosure frameworks based on industry feedback, including more comprehensive operational metrics, fill rate transparency, and infrastructure concentration patterns. Enhanced disclosure would improve both market oversight and institutional routing optimization.

The venues are innovating. The infrastructure exists. The measurement frameworks are available. What remains is coordinated adoption—transforming 44.3 billion shares monthly from opaque fragmentation into transparent, optimizable execution infrastructure.

I. THE MEASUREMENT PROBLEM

Asset managers overseeing trillions in capital face a deceptively simple challenge: determining which Alternative Trading Systems (ATSs) actually improve execution quality versus those that merely fragment liquidity and add operational complexity.

The obstacle isn't data scarcity, but an infrastructure gap masked as opacity. Buy-side firms cannot connect parent-order intent to routing decisions to venue-specific outcomes. Without this data lineage (complete audit trail connecting parent orders to venue outcomes), even sophisticated transaction cost analyses (TCA—post-trade measurement of execution quality) remain superficial rather than causal.

Consider the scale: 33 registered NMS Stock ATSs execute approximately 44.3 billion shares monthly, representing roughly 12.8% of total U.S. equity volume. Yet few institutional desks can isolate which venues demonstrably improve fill quality, protect information, or reduce market impact. Most depend on broker-reported markouts (post-trade price movement measuring execution quality) that conflate routing choices with venue effects.

The result: billions in execution alpha remain unmeasured and therefore uncaptured.

September data show that ATS participation is far from evenly distributed. Among the 50 most-traded equities, activity is heavily concentrated in a small subset of venues, while the remainder capture only fractional flow. The pattern varies by symbol, reflecting how broker routing preferences and liquidity segmentation drive uneven venue attribution (Appendix A, Figure 4).

The 2025 Market Landscape

Off-exchange venues have consistently handled more than half of U.S. equity volume throughout 2025. This structural pattern is particularly pronounced in Tape C securities (Nasdaq-listed), where off-exchange execution regularly captures 50-55% of total volume.

Figure 1 - Exchange vs. Off-Exchange Volume by Tape, H1 2025 (January-June) – Public Availability via CBOE Advantage

In H1 2025 (January-June), U.S. equity markets averaged 346.9 billion shares monthly. Exchanges accounted for 49.8% (172.9B shares), while off-exchange venues comprised 50.2% (174.0B shares). Beneath this headline split lies a critical structural divide:

Figure 2 - Off-Exchange Flow Bifurcation

Why This Bifurcation Matters

These ecosystems operate under fundamentally different competitive logics. Institutional ATSs compete on innovation and fairness mechanisms such as how orders interact, randomization windows function, and adverse selection (trading against better-informed counterparties) is mitigated. Retail wholesalers optimize price improvement and internalization throughput, operating primarily through payment-for-order-flow arrangements between retail brokers and wholesale market makers which is a distinct market structure dynamic beyond the scope of this analysis and primed for disruption.

This bifurcation clarifies why a single "off-exchange" statistic obscures more than it reveals. Institutional dark pools function as a separate, innovation-driven market layer demanding its own measurement framework.

Where Innovation Concentrates

Mehmet Kinak, Global Head of Equity Trading at T. Rowe Price, articulates the fragmentation challenge directly:

"The market in general—it's too fragmented. What we saw from 2005 to 2020 was a lot of proliferation of venues, but with very little innovation. IEX was one venue that came in and said, let's try something different. More recently we've seen innovation / a unique approach from venues like IntelligentCross, OneChronos, PureStream, and AlphaX."

Analysis of the 33 registered ATSs reveals why this assessment resonates: approximately 74.5% of off-exchange volume routes through retail wholesalers, while 25.5% executes through institutional ATSs offering variations on continuous midpoint matching or genuinely novel flows through venues with genuinely novel temporal extensions, probabilistic batch mechanisms, or ML-driven timing optimization.

The Attribution Deficit That Costs Billions

The challenge runs deeper than connectivity. Asset managers measure placement-level performance, potential through “Wheels”, whether VWAP algorithms achieved benchmark, whether arrival price strategies minimized shortfall. When placement performance looks acceptable, the underlying components remain opaque.

But "good" placement performance is not necessarily "optimal" placement performance.

Dr. Harry Feng, Managing Director and Global Head of Markets Research at BlackRock, frames the measurement imperative:

"Conditional liquidity and hosted rooms are only as valuable as our ability to measure how much alpha they preserve."

That statement encapsulates the current challenge: innovation exists within the institutional ATS segment, but measurement infrastructure lags. Without venue-level attribution separate from placement performance, institutions cannot determine which ATSs contributed to positive outcomes versus which simply added fragmentation.

Industry practitioner consensus estimates approximately a range from 80 to 95% of institutional routes to ATSs never result in fills—yet those non-fills carry information value that remains unmeasurable when brokers control both routing logic and performance reporting. A venue with a 3% fill rate might be poorly designed or expertly protecting its liquidity pool from informed traders. Without granular data, these scenarios are indistinguishable.

Moreover, the 80 to 95% non-fill rate creates an information leakage vector: sophisticated participants can deploy minimal-size probes across venues to infer institutional order presence through response latencies and rejection patterns. These "pinging" strategies exploit venue mechanics never designed for anti-gaming, transforming fairness features into inadvertent directional signals.

The Hidden Cost of Invisible Routes

Consider a deceptively simple question: Does routing transparency require visibility into unfilled orders, or only executed trades? Some practitioners dismiss unexecuted routes as noise—"Fill rates don't matter; non-executions cost nothing."

This perspective misses the information content in placement decisions. Every route carries timing, intent, and venue selection logic. The absence of a fill doesn't eliminate market impact: each placement affects queue dynamics, reveals urgency signals, and creates opportunity cost.

Without visibility into all routing attempts, buy-side desks cannot:

Detect broker router bias toward affiliated venues

Measure venue selection sequencing and priority logic

Quantify information leakage from unfilled IOIs

Validate that routing truly optimized for their objectives

The venues succeeding long-term will be those offering explainability across both executed and unexecuted flow—proving their value proposition extends beyond fills to comprehensive routing intelligence.

The cost of this opacity: roughly $11 billion annually in addressable execution improvements that incomplete venue transparency leaves uncaptured.1

This report examines how infrastructure providers, technology platforms, and venue innovators are closing that gap not through regulatory mandates, but through transparency infrastructure that makes differentiation measurable and innovation economically rewarding. The analysis throughout this paper is grounded in a close review of regulatory Form ATS-N filings, supplemented by direct conversations with ATS operators, institutional brokers, and industry leaders who shape and interpret venue design.

II. THE INNOVATION TAXONOMY: WHY MOST DARK POOLS LOOK IDENTICAL

In financial market microstructure, a taxonomy classifies the entire transactional ecosystem whether venues, order types, routing logic, participant segmentation, matching mechanics, and infrastructure as an interconnected system rather than isolated components. Execution quality emerges from how these elements interact: a venue's matching innovation means little without routing logic that recognizes when to use it, segmentation that determines counterparty quality, and infrastructure that supports fairness mechanisms.

This systemic view enables empirical evaluation of what drives execution outcomes. Within this broader framework, venue innovation represents a critical dimension. Without standardized venue classification, practitioners perform bespoke evaluation for each of 33 ATSs, driving routing decisions by broker relationships rather than measured differentiation.

A practitioner-oriented taxonomy distinguishes four innovation tiers:

Tier 1 — Structural Innovation Interactive Chart

Tier 2 — Sophisticated Segmentation (~42% of ATS volume)

Defining characteristic: Advanced participant classification using mark-out analysis, multi-tier scoring, or dynamic recategorization without altering core continuous matching mechanics.

Examples:

UBS ATS 13.0% — 5-tier participant classification

Sigma X2 8.6% — Mark-out based segmentation

MS Trajectory Cross 5.9% — VWAP interval-based matching

MS Pool (ATS-4) 5.3% — Continuous with size priority

JPM-X 3.3% — 5-tier dynamic recategorization

Barclays ATS 3.3% — Multi-tier segmentation

Morgan Stanley pools combined: 11.9%

These venues provide measurable value through adverse selection (trading against better-informed counterparties) protection, using quantitative metrics to classify participants into tiers.

Tier 3 — Standard Segmentation(~14% of ATS volume)

Defining characteristic: Basic participant tiers (institutional vs. conditional, firm vs. IOC) without advanced scoring.

Examples:

BIDS Trading 5.3%

IBKR ATS 2.8%

POSIT 1.7%

CBX 1.4%

Binary or simple classification without performance-based updates, often serving mid-cap and small-cap flow.

TIER 4 — Minimal Differentiation(~11% of ATS volume)

Defining characteristic: Continuous midpoint matching with price-time priority and limited differentiation. Exist primarily due to broker operational preferences, legacy connectivity, or internal client crossing.

Examples:

Instinct X 6.1%

Virtu MatchIt 2.6%

CrossStream 2.6%

The Concentration Pattern

Top institutional ATSs show varying concentration in highly liquid large-cap securities (NMS Tier 1 stocks) versus smaller stocks (NMS Tier 2):

IntelligentCross 58.0% NMS Tier 1 / 42.0% NMS Tier 2

PureStream 64.2% NMS Tier 1 / 35.8% NMS Tier 2

UBS ATS 60.3% NMS Tier 1 / 39.7% NMS Tier 2

Level ATS 63.4% NMS Tier 1 / 36.6% NMS Tier 2

This validates that matching innovation matters most in S&P 500, Russell 1000, and liquid ETF names—exactly where institutional flow values adverse selection (trading against better-informed counterparties) protection and information leakage prevention.

Figure 3: Institutional ATS Market Share by Innovation Tier (Q1 + Q2 2025)

Interactive color-coded market share distribution across all 33 registered ATSs, showing concentration of volume in Tier 1 structural innovators (blue), Tier 2 sophisticated segmentation (purple), Tier 3 standard segmentation (light blue), and Tier 4 minimal differentiation (red). Stacked bars display Tier 1 and Tier 2 security volumes within each venue's total market share. Top 5 venues capture 55.2% of market share, while 28 venues compete for the remaining 44.8%. Source: FINRA ATS Tier 1 & Tier 2 Reports, 265.8B shares analyzed across Q1 and Q2 2025.

The Consolidation Imperative

The visualization makes the consolidation pressure immediately apparent: IntelligentCross alone (16.1%) exceeds the combined share of the bottom 23 venues. This concentration pattern isn't random, but it reflects institutional routing logic responding to measurable differentiation when transparency infrastructure enables comparison.

The taxonomy reveals an uncomfortable truth: approximately 73.7% of institutional ATS volume executes through Tier 1 and Tier 2 venues, while the remaining 26.3% distributes across Tiers 3 and 4. The market share distribution exposes the pressure: top 5 venues capture 51.4%, while 28 venues compete for the remaining 48.6%. Twenty-three venues collectively handle less than IntelligentCross alone

This concentration reflects institutional routing responding to measurable differentiation. Flow concentrates toward:

Tier 1 structural innovation with empirically verifiable fairness mechanisms

Tier 2 segmentation leadership with quantifiable adverse selection (trading against better-informed counterparties) protection

Operational integration for specific use cases (block crossing, conditional execution)

Market forces are driving consolidation across three dimensions:

Tier 4 attrition: Venues with sub-1% market share cannot justify fixed costs of ATS operation. Ten venues handle less than 0.5% share each—economically unsustainable as measurement infrastructure exposes their lack of competitive advantage.

Tier 3 rationalization: Standard segmentation venues must demonstrate unique value. Those serving specialized niches (block trading in mid-caps) will survive. Generic segmentation will consolidate.

Broker consolidation: Multiple broker-dealers operate 2-3 separate ATSs with overlapping participants and similar mechanics. Economic pressure favors consolidating into unified platforms with sophisticated segmentation, reducing regulatory overhead while maintaining internalization capacity.

As Mehmet Kinak observed, the proliferation from 2005-2020 produced fragmentation without innovation. That fragmentation is reversing, accelerated by transparency infrastructure that makes commodity matching economically unrewarding.

Why This Taxonomy Matters

Mehmet Kinak emphasizes standardized classification:

"It'd be helpful to get the industry using the right terminology. Everyone calls things batch auctions or delay mechanisms, but the nomenclature isn't consistent. Your taxonomy idea helps people differentiate very quickly and show the excessive fragmentation taking place."

When venue characteristics are measurable and consistently classified, participants can assess whether structural innovations deliver execution quality improvements. The taxonomy reveals the innovation concentration challenge: only approximately ~32% of volume executes through venues with Tier 1 structural innovation.

III. INFRASTRUCTURE ENABLERS: RELIABILITY AS FOUNDATION FOR INNOVATION

Every innovation depends on infrastructure that never fails. MEMX established that benchmark not as a trading venue, but as an infrastructure provider powering other venues' innovation through Market-as-a-Service (MaaS) technology.

David Mellor, Managing Director at MEMX, frames reliability as non-negotiable:

"The most important thing to our clients undoubtedly is reliability. That is a non-negotiable. 100% uptime is 100%. Now let's talk about the other stuff."

This philosophy, resilience before innovation, forms the foundation upon which venues like Blue Ocean Technologies build temporal extensions that would be operationally impossible without exchange-grade infrastructure.

The MaaS Model: Converting CapEx to Elastic OpEx

The Market-as-a-Service model's value becomes clear when examining the traditional binary choice: building proprietary infrastructure (requiring $40-50 million in initial capital plus $10-15 million annually) or licensing existing technology (gaining efficiency but constraining differentiation).

MEMX offers a third path. Its ATS platform provides exchange-grade matching engine technology, dynamic capacity scaling, operational monitoring, regulatory compliance support, and continuous performance optimization, structured as partnership rather than transactional vendor relationship.

David Mellor, describes the capacity model:

" We expand with them as their need grows... it's much more of a dynamic conversation around what the business requires."

This eliminates the infrastructure trap where venues must either over-provision expensive capacity for hypothetical growth or risk hitting performance ceilings. For institutional ATSs competing in a segment representing roughly 12 to 16% of total market volume, the economic case for proprietary infrastructure is challenging. By converting CapEx into elastic OpEx, MEMX enables smaller ATSs to achieve exchange-grade reliability while focusing capital on matching innovation.

Case Study: Blue Ocean's 100% Uptime Achievement

The proof arrived in August 2024, when Blue Ocean Technologies migrated to MEMX's platform. Operating an overnight venue trading thousands of securities when primary markets are closed presents unique infrastructure challenges of managing NBBO formation without traditional market maker support, coordinating with Asian and European market hours, maintaining resilience when backup support is limited.

Post-migration results validated the MaaS approach completely. Mellor notes:

" Subsequent to them moving to our technology, its been smooth sailing from an operational standpoint. They are growing, and they have great plans going forward."

Blue Ocean's CEO Brian Hyndman confirms:

"Since we rolled MEMX technology in August of 2024, we had 100% uptime. We couldn't be happier with the exchange-grade technology that we selected."

For a venue handling significant volume during non-traditional hours, reliability represents more than operational convenience—it provides the institutional confidence required for adoption. MEMX’s exchange-grade infrastructure and Market-as-a-Service (MaaS) model deliver the resiliency, capacity, and uptime essential for markets operating beyond traditional hours. By leveraging this framework, Blue Ocean could focus on building liquidity and validating the viability of overnight trading without the friction of maintaining complex infrastructure. The MaaS model lowers barriers to temporal and structural experimentation, enabling venues to test and scale innovative market structures with enterprise-level stability from inception

IV. THE TRANSPARENCY LAYER: CONNECTIVITY THAT MEASURES

Transparency begins not with matching engines but with connections and critically, with high-fidelity data capturing the complete order lifecycle, not just fills. For years, the opaque link between buy-side order management systems and trading venues has been controlled by brokers who determine routing destinations and timing. That dependency is breaking down.

Fidelity Service Bureau (FSB) operates as a broker-neutral technology platform letting asset managers connect directly to institutional ATSs while maintaining full data lineage. FSB is not a broker but an infrastructure providing connectivity, data normalization, and analytics without executing trades or making routing decisions.

Solving the Technology Budget Problem

The technology barrier compounds the transparency challenge. Building infrastructure to optimize venue routing across 33 ATSs and measure comparative performance requires substantial ongoing investment in proprietary algorithmic technology of which budgets that only the largest asset managers justify.

Jared Kovach, head of product at FSB, quantifies the problem:

"Buy-side firms have access to all this liquidity. What they don't have is the technology budget to optimize it. It can cost $20 or $30 million a year to run an internal algo stack. That's what we solve—turning fragmentation into choice."

Jason Hughes, FSB's Head of Electronic Trading Sales, frames the accessibility challenge:

"When clients talk about inaccessible liquidity, we believe there is a portion of liquidity that is inaccessible via a traditional broker algo. Using a technology solution like FSB, goes a long way towards eliminating accessibility issues, and brings the focus to optimization of liquidity. From there it just becomes a question of build, which can be very expensive, versus buy."

For most institutional investors, venue optimization and routing control remain inaccessible despite their importance to execution quality. Mid-sized asset managers lack the technology budgets to build sophisticated ATS evaluation frameworks, leaving them dependent on broker routing logic that may not align with their execution objectives.

The Architecture: Sponsored Broker Connectivity

FSB's architecture operates through sponsored broker connectivity: FSB manages the technology layer connecting to sponsored brokers' pipes, handling data normalization and analytics infrastructure, while institutions select which brokers provide actual market access to specific ATSs.

Kavy Yesair, Head of Electronic Trading at FSB, explains the multi-broker flexibility:

" The goal of Fidelity Service Bureau is to access liquidity as close to the point of origination as possible. Absent that, when it comes to Broker Sponsored venues, Directed Access or Smart Order Routers, I'll say to clients, which broker do you want to use? Clients can put these on wheels and use that as a way to direct payment to brokers of their choice.”

The flexibility matters because different brokers access different segments of the institutional ATS landscape. FSB's multi-broker architecture lets institutions access the full spectrum while maintaining unified measurement which is particularly important given market share concentration where institutions need ability to evaluate whether smaller Tier 1 innovators deliver better execution quality than larger Tier 2 venues.

Performance Attribution Across Three Dimensions

FSB's analytics platform addresses the attribution deficit through performance scoring across multiple dimensions: execution quality, liquidity access, and venue uniqueness.

Yesair explains the peer benchmarking capability:

"We actually say to the customer, here's your score. How do you look versus the collective community?"

This peer benchmarking enables institutions to evaluate whether their execution quality across institutional ATSs matches, exceeds, or lags comparable firms, measurement impossible when brokers control both routing and performance reporting.

The uniqueness measurement particularly addresses institutional ATS differentiation challenges. Rather than assuming all 33 ATSs provide similar liquidity, FSB quantifies whether a venue offers access to genuinely different counterparties or simply replicates executions available through alternative routes. This captures whether Tier 1 venues like PureStream or IntelligentCross deliver structural value beyond what Tier 2-4 continuous midpoint pools provide.

The Clean Data Sequence

Yesair articulates FSB's foundational philosophy:

"To get good data, you need clean data. Using bilateral segmented liquidity sourcing gives you the cleanest set. Then you can create transparency—and with transparency, optimization. That's the sequence—clean data, transparency, optimization."

This three-stage framework mirrors how effective institutional ATS evaluation must operate:

Clean data: Establish data lineage (which orders went where, exact routing timestamps)

Transparency: Enable transparent measurement (comparative venue performance)

Optimization: Route more flow to genuinely differentiated venues based on empirical evidence

Without the first stage, subsequent stages become impossible.

A Framework for Causal Attribution: Beyond Correlation

The estimated 80 to 95% non-fill rate reveals why traditional venue evaluation fails: most analyses measure correlation, not causation. A venue might show strong fill rates and favorable markouts but is that because the venue delivers superior execution quality, or because brokers route easier orders there while sending complex flow elsewhere?

Traditional TCA suffers from three fundamental limitations that a causal inference framework could address:

Confounding variables: Market volatility, spread dynamics, and order size affect outcomes independently of venue quality. Propensity score matching techniques could compare similar orders routed differently, isolating genuine venue effects from selection bias.

Venue routing remains one of the most opaque and differentiated aspects of broker execution. Each broker designs its routing logic uniquely with some maintain static routing waterfalls updated periodically, others employ adaptive, real-time optimization engines, and many outsource routing decisions to third-party smart order routers. The precise sequencing, prioritization, and conditions triggering venue selection are often proprietary and undisclosed.

Sequence dependencies therefore matter: the fifth ATS in a routing waterfall updated weekly operates under fundamentally different liquidity conditions than the first. A complete routing tree that captures every attempt, timestamp, and rejection would enable sequence-aware evaluation—revealing each venue’s marginal contribution to execution quality and its role within the broker’s adaptive decision network.

While much of Marcos López de Prado’s work focuses on portfolio construction and factor investing, the core principle carries into execution analysis. As he writes, “Absent a causal theory, findings are likely to be spurious artifacts of backtest overfitting and incorrect model specification choices.” In the context of venue evaluation, associational metrics—like post-trade markouts—can misrepresent a venue’s value by ignoring broker-specific routing logic, rejection paths, and the timing of intervention. Without a causal model to isolate these effects, attribution risks reinforcing structural opacity instead of surfacing genuine marginal contribution.

Intent alignment: Not all midpoint ATSs serve the same purpose. Some routes represent "intentional flow" from the broker that has high-confidence executions where liquidity is known and just wants a mid-point fill. Others represent "opportunistic flow" or exploratory routes testing whether structural innovations extract liquidity when continuous matching fails or result in adverse selection (trading against better-informed counterparties).

A venue showing 15% fill rates on opportunistic flow during volatile conditions may deliver more alpha than a venue showing 40% fill rates on intentional flow during calm periods. Traditional metrics cannot distinguish these scenarios. Causal attribution frameworks could.

This approach transforms the estimated 80 to 95% non-fill problem from measurement noise into strategic intelligence:

Did the non-fill occur because the venue optimized for potentially toxic flow? Sophisticated adverse selection (trading against better-informed counterparties) protection—a positive signal.

Did the non-fill occur during unfavorable quote conditions? Routing logic needs refinement, not venue underperformance.

Did the non-fill occur because participant base doesn't match order characteristics? Better venue selection mapping needed.

The causal framework also validates the Tier 1-4 taxonomy: different venue types excel when evaluated against their actual use cases. Tier 1 innovators demonstrate value on opportunistic flow during volatility. Tier 2 segmentation leaders demonstrate value through adverse selection (trading against better-informed counterparties) protection. Without causal inference methodologies, these distinctions remain invisible.

This represents the next evolution in execution quality measurement: moving from "which venues filled orders" to "which venues aligned with intent" to "which venues delivered measurable alpha given conditions and sequence." This is the measurement infrastructure that makes genuine innovation economically rewarding and not through what platforms currently implement, but through frameworks the industry could adopt to transform routing data into causal intelligence.

The Probing Problem: When Transparency Enables Gaming

The venue probing challenge introduced in Section I, where minimal-size orders infer institutional presence, becomes more acute when transparency infrastructure provides granular routing data. The same complete routing lineage necessary for causal attribution (every venue attempt, timestamp, rejection) creates feature-rich datasets for adversarial machine learning.

Quantitatively-driven participants can deploy systematic odd-lot probes across ATSs, treating venue response patterns as Bayesian signals: a 3ms fill from Venue A followed by 7ms fill from Venue B, combined with specific order type interactions, may statistically correlate with large institutional order presence. Sequential routing behaviors, fill probability distributions, and even randomization window variations become exploitable information channels.

This gaming vector represents a fundamental tension in transparency design: complete routing lineage enables legitimate causal inference for buy-side optimization, but also provides training data for adversarial models designed to detect institutional flow signatures and predict directional intent. Venues like IntelligentCross that employ ML-driven fairness must extend their models beyond market conditions to detect game-theoretic probing patterns where the venue itself becomes the signal rather than the market.

The Historical Context: Six Years of Advocacy

The transparency imperative isn't new. A 2019 paper, "Venue Analysis Holy Grail: Routing Transparency Initiative,"2 advocated for standardized intent-based routing taxonomies that would enable empirical venue evaluation. The core argument: without capturing why orders were routed to specific venues, performance attribution remains fundamentally flawed.

The paper warned about exactly what we now quantify as the estimated 80 to 95% non-fill problem: "We cannot analyze venue performance in a vacuum—routing intent and sequence context are essential." When most routes never fill, those non-fills contain critical information about matching logic and adverse selection (trading against better-informed counterparties) protection but only if we know the routing intent and sequence context.

Six years later, that vision is becoming reality. What changed:

Computational economics transformed: Cloud computing infrastructure, GPU acceleration, and distributed processing converted what was economically prohibitive in 2019 into commodity capability in 2025. The full enriched routing dataset with every venue attempt, timestamp, rejection reason, sequence position can generate terabytes of granular data that only the largest firms could store and analyze six years ago. A senior technology executive at a leading market maker dismissed the routing transparency concept in 2019, noting the dataset would be "enormous and noisy and economically unviable for most participants." That assessment was correct then. Today, with ML/AI frameworks purpose-built for high-dimensional, noisy financial data, the noise has become the signal. Pattern detection algorithms can now extract causal relationships from routing sequences that appeared as statistical noise under traditional regression approaches.

Technology maturity: Platforms like FSB now provide the analytics infrastructure that was missing in 2019, with potential to implement causal attribution frameworks through intent-tagged routing data, propensity matching, and sequence-aware evaluation. What required $20-30 million annual technology budgets now operates as managed service infrastructure accessible to mid-sized asset managers.

Regulatory evolution: Regulators increasingly prioritize transparency and auditability across market structure, creating pressure for standardized routing disclosure and venue-level performance data. This regulatory attention transformed routing data from proprietary competitive information into infrastructure-level expectation turning compliance obligation into competitive advantage for venues willing to explain their mechanics and enable empirical comparison.

The 2019 RTI framework proposed classifying routing decisions by urgency, liquidity type, sequence context, and expected outcomes enabling venues to be evaluated against their intended purpose rather than aggregated statistics. This directly informs the Tier 1-4 taxonomy: different venue types excel when evaluated against their actual use cases.

What remains unfinished: broker adoption of standardized intent codes varies widely, real-time feedback loops remain largely batch-oriented, and complete routing disclosure is limited by competitive concerns. But the infrastructure now exists to close these gaps. The routing transparency initiative is no longer advocacy, it's becoming infrastructure.

Neutral Access: Transient Liquidity Philosophy

Jason Hughes, describes the platform's routing philosophy:

"We represent client orders everywhere because liquidity is transient. Our job isn't to overweight one venue over another but to help clients see their performance across venues."

This neutrality is critical given the institutional ATS landscape. With ten venues capturing over 50% of market share, there's natural pressure for brokers to favor high-volume venues where fill probability is highest. But fill probability doesn't equate to execution quality.

FSB's broker-neutral architecture enables institutions to evaluate whether smaller Tier 1 innovators deliver better execution quality than larger continuous midpoint pools, even if fill rates are lower—transforming innovation into accessibility by ensuring advances in matching logic reach the institutions who matter most.

V. VENUE INNOVATIONS: FOUR STRUCTURAL ARCHETYPES

The venues examined represent four distinct approaches to structural innovation within the institutional ATS landscape. Each addresses a different dimension of the transparency gap: temporal extension, deterministic fairness, probabilistic matching, and cross-border governance.

A. Blue Ocean: Temporal Extension as Infrastructure

From 8 p.m. to 4 a.m. ET, when most U.S. markets sleep, Blue Ocean Technologies connects U.S. equities to Asian and European price discovery. Operating on MEMX's infrastructure platform, Blue Ocean has become the first regulated bridge across global trading sessions.

John Willock, Blue Ocean's Chief Strategy Officer, describes the scale:

"We trade close to 5,000 different names every night—not just megacaps. In some cases, overnight spreads are tighter than daytime SIP spreads."

Five thousand names. That statistic challenges assumptions that after-hours trading is limited to a small cohort of high-volume securities. Blue Ocean demonstrates that meaningful overnight liquidity exists across a broad universe—and that institutional participants will engage when infrastructure and transparency support it.

Transparency as Competitive Advantage

The transparency aspect distinguishes Blue Ocean from most institutional ATSs. Unlike dark pools, Blue Ocean operates a fully transparent displayed order book.

Matt Brown, Blue Ocean's Sales & Trading Director, emphasizes this architectural choice:

"You've got to disabuse people of the notion that an ATS is dark. We put out data; we have a visible book."

This transparency enabled empirical validation of overnight execution quality that dark pool operators traditionally do not provide. The displayed book model matters for institutional adoption: trading desks evaluating overnight execution can assess available liquidity before committing orders, reducing information leakage concerns that plague dark pool interaction.

September 2025 Performance Validation

Analysis of H1 2025 trading data confirms Blue Ocean's value proposition. The overnight session demonstrated strong directional accuracy, with the majority of trades aligning with next-day market moves confirming efficient capture of overnight drift. Overnight participation remained stable at 200-450 symbols exceeding $200K per session, with consistent breadth across the month.

Event-driven bursts occurred on Mondays and mid-month Thursdays coinciding with macro or earnings releases, with peak volume reflecting retail and institutional responsiveness to information events. The return profile showed frequent small gains and losses punctuated by rare, large positive jumps characteristic of informed flow capturing asymmetric opportunities. The captured versus uncaptured alpha pattern demonstrated proportional, low-noise behavior typical of day order flow.

Blue Ocean's overnight session demonstrated consistent directional success, broad participation, and robust performance under jump-driven, event-sensitive market conditions reinforcing its role as a credible and efficient early liquidity venue bridging U.S., Asian, and European trading sessions.

Workflow Integration: The Bloomberg Breakthrough

The Bloomberg integration represented the workflow breakthrough transforming overnight trading from specialized tool to integrated execution option. Brown called it:

"A breakthrough in workflow integration—it puts overnight liquidity right beside daytime execution."

Before this integration, overnight trading required separate workflows, different systems, and manual coordination. Bloomberg's integration made overnight liquidity visible within existing OMS/EMS infrastructure, removing the primary adoption barrier.

Blue Ocean's evolution demonstrates that temporal innovation succeeds when three elements align: infrastructure reliability (MEMX), workflow integration (Bloomberg), and transparency (displayed order book).

B. PureStream: SIP-Referenced Streaming Liquidity

PureStream's innovation reframes execution by transforming discrete order events into continuous liquidity streams with bilateral, real-time agreements between participants to trade dynamically in sync with the public market tape.

A stream forms when two counterparties agree to interact within overlapping liquidity parameters defined by a Liquidity Transfer Rate (LTR)—the percentage of market volume they are willing to participate in. The matching event itself triggers the stream, not the reference trades. Once matched, orders move from the order book to a "matched book" where they remain paired and synchronized until completion.

COO Sean Hoover summarizes the concept:

"We're not matching orders in the traditional sense—we're matching intent. Two firms agree to transfer liquidity continuously, synchronized with the tape. Every market print becomes an opportunity to fulfill that agreement."

The Two-Book Architecture: Match First, Then Reference

PureStream operates with two distinct books that separate matching logic from execution:

Order Book: Where orders await matching based on LTR parameters and quantity

Matched Book: Where matched order pairs reside, receiving continuous fills synchronized to SIP reference trades

The sequence is critical: the match occurs first between two orders, triggering a "stream on" message to both participants. Only after this matching event do reference trades begin generating fills. The match is the trigger—reference trades are the fulfillment mechanism.

This architecture removes the traditional provide/take asymmetry by synchronizing both sides to the same market reference. Each participant simultaneously contributes and consumes liquidity under identical, deterministic rules. Execution is governed by the agreed Liquidity Transfer Rate and verified SIP prints—not by order arrival time or queue position.

Real-Time Referencing: No Time Windows, No Averaging

Unlike time-weighted average price mechanisms, PureStream executes fills in real-time as each reference trade prints to the SIP. There is no execution window and no averaging calculation—each fill executes at the actual reference trade price:

First reference trade prints → Both matched orders receive that fill at the reference price, plus cumulative execution rate

Second reference trade prints → Both orders receive that fill at the reference price, plus updated cumulative rate

Process continues → Each SIP print generates immediate fills until one order exhausts its limit, quantity, or cancels

When fills reach 20+ shares, they report immediately to the tape. Smaller fills accumulate until reaching the 20-share reporting threshold. This real-time execution model means a stream typically contains many individual trades, each priced at the actual reference trade rather than calculated averages.

CEO Armando Diaz explains:

"Once matched, both sides receive the same verified reference—a single version of truth."

Example: Stream Execution Flow

Interactive Visualization: View PureStream LTR Flow Animation →

Each fill executes at the actual reference price in real-time. The matched orders remain in the matched book, receiving continuous fills synchronized to market activity, until a "stream off" message terminates the stream when quantity is exhausted or one party cancels.

Deterministic Matching, Non-Deterministic Price Discovery

The streaming model achieves determinism through LTR commitment and bilateral matching—both counterparties agree to the same volume participation rate and remain matched throughout execution. This is deterministic matching.

Where non-determinism emerges is in price discovery: matched participants don't control where reference trades occur (near/mid/far). Reference trade distribution follows market dynamics—typically 50% near/far, 20% mid, with the balance at other price points. Participants agree to accept this probabilistic price distribution as the cost of continuous, synchronized execution. The counterparty isn't picking the "spot" to trade—both sides accept whatever reference trades the market generates. While many traditional ATSs aim for low-impact midpoint execution with potential size advantages, they often struggle to distinguish between firm interest and fleeting participation. PureStream addresses this by introducing Liquidity Tolerance Ranges (LTRs), where execution probability scales with displayed volume commitment. Participants signaling higher tolerance for size receive proportionally higher fill rates, shifting incentives toward meaningful liquidity provision rather than opportunistic, low-size probing.

Market Validation Through Concentration

Like other Tier 1 innovators, PureStream demonstrates meaningful concentration in liquid securities: 64.2% of volume executes in Tier 1 stocks (S&P 500, Russell 1000 large caps), with 35.8% in Tier 2 names. This concentration pattern validates the streaming model's value proposition—in highly liquid securities with continuous market prints, volume-synchronized matching provides differentiation from continuous dark pools while maintaining broader participation than pure large-cap venues.

The 3.7% market share, while smaller than IntelligentCross's dominance, represents meaningful institutional adoption for a fundamentally different matching paradigm. Participants don't route to PureStream for speed or opportunistic fills—they commit liquidity streams because deterministic volume participation provides execution certainty that continuous matching cannot guarantee.

Where IntelligentCross achieves determinism through ML-driven timing and Blue Ocean through temporal extension, PureStream achieves it through SIP-referenced synchronization. Both counterparties commit to the same reference trade stream—eliminating the provide/take asymmetry that characterizes traditional dark pool interaction.

C. IntelligentCross and Imperative Execution: A Platform for Structural Market Innovation

Roman Ginis, founder of Imperative Execution and architect of IntelligentCross, treats fairness as a timing problem. The result: IntelligentCross leads the institutional ATS market with 16.1% share with the strongest empirical validation that matching innovation matters more than broker-dealer scale or embedded relationships. But IntelligentCross represents just one component of a broader platform engineering superior execution outcomes through structural innovation.

The Core Innovation: ML-Driven Timing Optimization

IntelligentCross's matching engine analyzes real-time market microstructure with quote update frequency, spread volatility, message traffic patterns, historical stability to dynamically calibrate randomization windows (Imperative Execution ATS-N Filing). For ASPEN's displayed book, these windows operate in microseconds (150–900 microseconds); for the Midpoint dark pool, they extend to milliseconds (up to 200 milliseconds). When conditions suggest information events, timing windows expand to prevent execution during exploitable moments. When stability emerges, windows compress to maximize fill rates while maintaining fairness.

Lorna Boucher, Chief Marketing and Communications Officer at Imperative Execution, describes the foundational philosophy:

"We really focused on the quality of the execution for both counterparties. Instead of just being a neutral crossing venue... we set up our system. We literally don't know who the counterparties are and neither of them has any additional information than anybody else. And it's a completely unpredictable time horizon and it's really, really tiny."

This architecture eliminates the need for participant segmentation which is a critical differentiation from Tier 2 venues. Where UBS ATS and Sigma X restrict interactions through classification tiers, IntelligentCross achieves equivalent adverse selection (trading against better-informed counterparties) protection through unpredictable timing that benefits all participants equally. The Minimum Resting Period (MRP) requiring orders to rest up to 200 milliseconds before matching neutralizes latency arbitrage by making speed advantages irrelevant. As Boucher emphasizes:

"In a marketplace where upwards of 70% of the flow is coming from market makers" (FINRA ATS Tier Summary, 2024), categorical exclusion becomes counterproductive—limiting liquidity without providing protection when orders inevitably meet those same market makers on exchanges.

The system continuously recalibrates in real-time through Intraday Optimization by performing over 66 million optimizations daily that have delivered 45,000 additional trades per day with zero post-trade markouts (1).

"The ML has worked even faster than we thought it would," Boucher explains. "This kind of calibration and optimization is like one of the best use cases for ML and AI, because it's not asking it to do anything other than crunch the data. And so it actually is quite effective and really, really fast."

The measurable results validate the approach: IntelligentCross's Midpoint book delivers 75% lower market impact than exchange midpoint executions, while early performance analysis showed post-trade markouts of just 0.13 basis points versus 1.37 basis points on exchanges—nearly ten times lower (2). This performance applies across billions of shares monthly, not cherry-picked samples. Boucher critiques selective reporting:

"Some people in the innovator category will run around and talk about markout rates, and they'll talk about how great they are. But when you look at the executed flow, it ends up being an incredibly small subset of flow... Is it actually accessible to everyone at that level of execution quality or not?"

Aspen: Displayed Trading and Price Discovery

Beyond midpoint matching, Imperative Execution's Aspen displayed book demonstrates that ATSs can outperform traditional exchanges in price discovery. Independent analysis by Pico found Aspen's quotes inside the NBBO more than 12% of the time, delivering average price improvement of 2.5 basis points. Separately, Exegy identified nearly 7 million instances daily where IntelligentCross provided superior displayed prices, with quotes 30% better than exchange spreads on average (3). Aspen maintains this performance with 96% quote availability for S&P 500 stocks.

When Reg NMS established thresholds for displayed versus dark trading, most venues chose to remain entirely dark. Ginis identified this as missed opportunity. As Boucher explains:

"Roman was looking at the quality of execution that we were having. And he said, in the right circumstances, if people are feeling comfortable about submitting orders that are displayed in our model, then why shouldn't we also offer a displayed book? Because it'll inform price discovery better."

Aspen operates three distinct limit order books (Fee/Fee, Maker/Taker, Taker/Maker), each with different economics and Market Identifier Codes, providing subscribers flexibility to align execution with strategy (Imperative Execution ASPEN ATS-N Filing).

Jumpstart: Buy-Side Direct Control

Jumpstart represents a structural innovation in bilateral execution—giving buy-side traders direct IOI control without exposing order flow to broker-dealer visibility. The architecture eliminates the principal-agent problem that plagued earlier IOI models:

"The buy side leaves no footprint that even their broker dealer can see unless they send a confirmation. And so there's no blotter scraping going on. There's no sense of like what's behind the IOI... The genuine element of choice is now we've actually given control and agency specific to these orders to the buy-side trader." (Boucher)

Buy-side traders generate IOIs directly from their EMS/OMS. These IOIs rest in hosted pools invisible to the sponsoring broker-dealer. When matching occurs, buy-side traders decide whether to firm up with the first moment the broker learns of the interest. This eliminates every information leakage vector that concerned institutions about previous IOI initiatives.

Broker-dealers customize their Jumpstart implementations. For example, Jefferies crosses early-stage algo flow with buy-side IOIs; others may use principal positions, passive orders, or bilateral client matching. Each implementation creates differentiated execution destinations rather than commoditized dark pool access.

The Validation: Market Leadership Through Innovation

IntelligentCross's market share trajectory starting from 21st in early 2020 to 9th by November 2020, doubling market share in 2021, and reaching 16.1% by 2025 proving genuine structural innovation can achieve dominant market position without broker-dealer captive flow (4). The platform serves over 90 broker-dealer subscribers and has received validation from leading institutions including Instinet, Bernstein, and Clearpool Group, with Dr. Nataliya Bershova of Bernstein noting "1.5 basis points of price improvement for our orders."

The 16.1% share exceeds both UBS ATS (12.9%) and Sigma X (8.1%), demonstrating that zero-segmentation ML-driven fairness outcompetes sophisticated participant classification when execution quality is measurable. This validates the paper's core thesis: matching innovation matters more than broker relationships.

The platform approach: IntelligentCross for midpoint, Aspen for displayed trading, Jumpstart for bilateral execution which provides execution optionality that single-venue dark pools cannot match. As Boucher notes on the industry's routing inefficiency:

"The amount of money that's left on the table or that's paid in lost price improvement or lost midpoint opportunities... think about how all that money filtering back into the hands of the investors."

Imperative Execution's success demonstrates that when venues engineer solutions to genuine market structure problems—adverse selection (trading against better-informed counterparties) through timing optimization, stale quotes through superior price discovery, information leakage through architectural barriers—institutional flow concentrates toward measurable differentiation.

D. AlphaX US: The Fast Auction Innovation

AlphaX US solves a fundamental tension in auction design: how to provide the fairness protections of periodic matching without the execution uncertainty that makes institutional algorithms hesitant to commit flow.

Heidi Fischer, President, TMX AlphaX US, frames the design challenge directly:

"We wanted to introduce an auction venue, but we wanted it to closely mimic a continuous trading market to give some of the protection of an auction, but not have orders stuck for long, because we know how frustrating that can be."

The solution: 10-millisecond collection periods with approximately one-microsecond execution windows.

The One-Microsecond Execution Window

While AlphaX US collects orders for 10ms intervals, the actual matching event executes in approximately one microsecond. Fischer explains:

"Our actual match event from the time we start running it until the time it's done generally takes about one mic. So you'll see in our ATS-N we say up to five to protect ourselves, but it's really closer to one mic in practice. And that is the only time your order is stuck in our venue. So you can send a firm order and not feel like it's going to just sit there waiting for too long, but still enjoy the benefits of the protection of an auction."

This architecture addresses the primary institutional concern about batch auctions: execution certainty. Orders aren't frozen for extended periods. The 10ms collection window provides auction fairness neutralizing latency advantages within each interval while the microsecond execution prevents the order-parking problem that plagues slower auction designs.

Pricing Innovation: Bilateral Price Improvement

AlphaX US' pricing methodology differentiates it from standard midpoint-only auction venues. Rather than executing all matches at NBBO midpoint, AlphaX US prices at the midpoint between the buyer's actual price and seller's actual price still constrained by NBBO but enabling price improvement for both counterparties.

Fischer describes the competitive advantage:

"A lot of people use these auction venues for their midpoint strategies, because that's the only price they're getting. And my opinion is we're taking away the opportunity for price improvement... What if someone's more passive or more aggressive, and they want to use our venue? Why shouldn't they have that opportunity?"

The mechanism creates bilateral price improvement: an aggressive order willing to cross the spread matches against a passive midpoint order, and both sides split the spread 50/50. Orders priced more aggressively than midpoint receive priority for matching against passive liquidity.

"Why go cross the spread out on exchange when you can come to us first and if there's a midpoint order sitting there, you're both going to split that price improvement 50-50."

Early adoption data validates the approach. Fischer notes that participants initially added AlphaX US to midpoint-only strategies but are now expanding to more aggressive order types as they observe the price improvement benefits: "When you get price improvement, you get really good price improvement, and you get price improvement a decent amount of the time on more aggressively priced orders."

No Maker/Taker Complexity

AlphaX US deliberately avoided maker/taker fee structures. Fischer explains the rationale:

"We don't have a concept of make or taker. Should the person who's been sitting there the longest be the maker? In an auction venue, that gets really confusing, hard to identify and hard for the person sending to identify. So we went with everybody's equal. There is no concept of maker-taker."

This equality principle aligns with the auction fairness model preventing priority gaming based on order timing or classification.

Performance Metrics: Institutional-Grade Fill Quality

Nine months post-launch, AlphaX US demonstrates meaningful institutional adoption:

127 shares average fill size—placing AlphaX US in the top half of all venues including block-focused ATSs

~30 participants (direct and indirect) connected, representing bulge bracket firms, other innovative brokers, and liquidity providers

The 127-share average fill size particularly validates that AlphaX US attracts substantial institutional orders, not just algorithmic penny-packets. Fischer emphasizes:

"That puts us in the top half of venues, and that includes all of the block venues... We're getting some really good chunky fills out there, partially from conditionals and partially from firm orders."

Analytics and Backtesting Infrastructure

AlphaX US leverages cloud-based analytics (AWS) for sophisticated performance measurement though the actual matching engine remains on dedicated hardware at Equinix NY5. The analytics platform enables participants to conduct counterfactual analysis:

"If a broker sent an order with certain parameters around it, or they sat for 15 seconds and cancelled, could they have gotten a fill if they sat for 30 seconds? We can tell you that. Did they sit for 15 seconds and everything we could get done was done after five and that was an opportunity cost lost? We can also tell you that."

This backtesting capability addresses the measurement challenge: institutions can evaluate whether parameter changes minimum execution quantities, counterparty segmentation, and duration would have improved outcomes.

TMX Backing: Startup Agility with Enterprise Stability

AlphaX US operates with a unique structural advantage: startup mentality backed by TMX Group's almost $10 billion market cap and 170+ year operating history. Fischer emphasizes the hybrid model:

"We very much have this startup mentality and we very much have built this venue as a startup, but with all of that support from a really large, smart parent company. There's a 10-year plan here. This is in front of investors. We're a publicly traded firm. This isn't a scenario where our funding could go away tomorrow."

This financial stability enables long-term innovation investment that pure startups cannot sustain. TMX's commitment extends beyond the current single-book ATS. Fischer confirms plans for a potential second book within the next year and exploration of additional asset classes and equity ATS models.

The Batch Auction Value Proposition

AlphaX US' periodic batch structure eliminates continuous matching exploits that advantage speed over size: time priority gaming disappears when all orders in a collection window receive equal treatment; latency arbitrage becomes impossible when matches occur at fixed intervals; quote fading strategies fail when market makers cannot cancel faster than auction execution.

Yet the auction model requires rethinking institutional routing logic. Smart order routers optimized for immediate continuous matching must adapt to evaluate whether committing orders for 10ms collection periods—with uncertain execution probability—delivers better outcomes than sequential venue testing. The 127-share average fill size and 30-participant adoption suggests institutions are making that evaluation positively, particularly for larger orders where auction fairness outweighs continuous speed advantages.

AlphaX US validates that batch auctions can achieve meaningful institutional adoption when execution speed approaches continuous markets, pricing methodology enables price improvement beyond midpoint-only matching, and enterprise backing provides the stability necessary for long-term routing optimization.

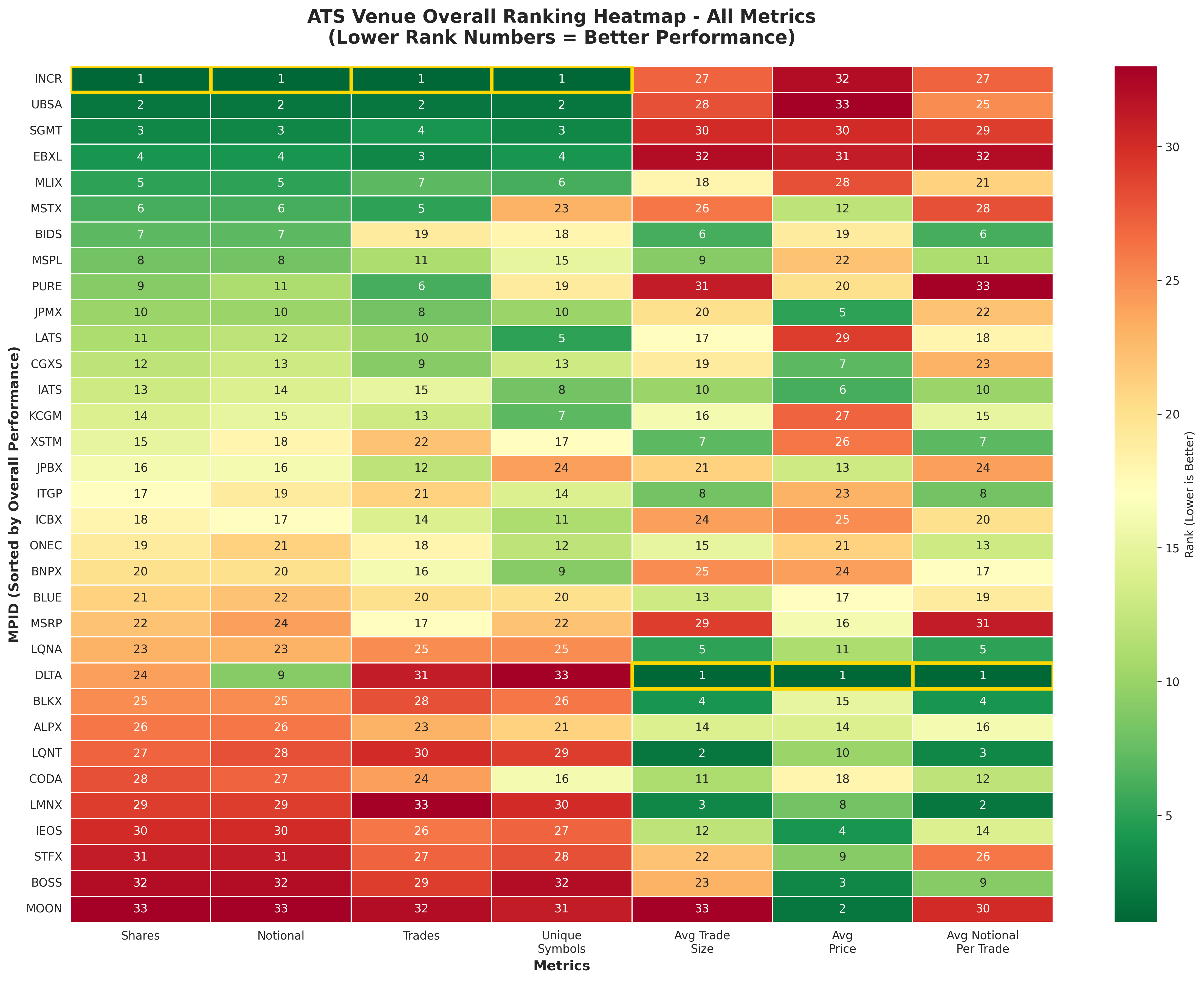

While these four venues represent the leading edge of structural innovation, they exist within a much broader and more heterogeneous ATS ecosystem. To contextualize their relative performance, Appendix A, Figure 5 (ATS Venue Overall Ranking Heatmap) visualizes ranking scores across multiple execution dimensions — total shares, notional volume, trade counts, symbol diversity, and average trade size — derived from normalized FINRA Tier 1 and Tier 2 data for 2025.

The heatmap confirms that differentiation remains limited across most ATSs. A small subset — including IntelligentCross, UBS ATS, and Blue Ocean — exhibits consistent strength across metrics, while the majority cluster in a narrow performance band. This pattern underscores a central finding of the report: venue proliferation has outpaced venue innovation.

(See Figure 5 in Appendix A for methodology.)

VI. BUY-SIDE PERSPECTIVES: THE MEASUREMENT IMPERATIVE

Even the most elegant venues cannot fulfill their potential without transparent access and measurable performance data. Buy-side firms are demanding explainability over speed as they navigate 33 ATSs.

As one Global Head of Trading states:

"I would like a lot more transparency."

This sentiment—consistent from bulge bracket to mid-sized firms—underscores that the transparency deficit affects the entire institutional ecosystem.

The Alpha Preservation Test

As Dr. Harry Feng observed in the introduction, the value of conditional liquidity and hosted rooms depends entirely on measurement capability. This principle extends to the broader institutional ATS landscape: institutions recognize that IntelligentCross uses ML-driven timing, Blue Ocean trades overnight, and PureStream matches on volume—but cannot easily determine whether those innovations improve execution costs by measurable basis points.

Without daily, strategy-level attribution data with fill rates by venue, mark-out analysis on routing intent, adverse selection (trading against better-informed counterparties) metrics, uniqueness scores with the gap between innovation awareness and performance measurement creates strategic paralysis. Traditional TCA measures outcomes without attributing causality, leaving institutions unable to distinguish genuine differentiation from marketing distinction.

The Simplification Imperative and Consolidation Pressure

Industry practitioners consistently express frustration with venue proliferation. The data validates this concern: 33 registered ATSs collectively handling over 40 billion shares monthly, yet the taxonomy reveals only approximately 32% executes through venues with Tier 1 structural innovation.

The fragmentation tax is measurable: each additional routing destination requires connectivity costs, operational monitoring, compliance oversight, and TCA resources. For mid-sized asset managers, evaluating 33 venues requires technology budgets they cannot justify. Even large institutions struggle to perform rigorous comparative analysis across the full venue universe.

Industry practitioners note that while venues may be operationally convenient for brokers, serving as additional destinations for internal flow, they impose evaluation complexity on institutional desks. This asymmetry creates a "fragmentation tax" where the buy side bears the cost of venue proliferation that primarily benefits broker operational efficiency.

Market forces are already driving consolidation. Tier 4 venues handling less than 1% market share cannot justify the regulatory compliance burden. Form ATS-N reporting, surveillance requirements, connectivity maintenance, and operational support create fixed costs that small venues cannot amortize across limited volume.

More critically, broker-run ATSs that function primarily as internalization facilities without genuine matching innovation face intensifying pressure. When these venues simply cross internal client flow using commodity midpoint matching, they provide minimal incremental value while imposing measurement complexity on institutional routers.

The data reveals the pressure: 23 venues collectively handle less market share than IntelligentCross alone. Operating an ATS requires substantial fixed costs of regulatory compliance, technology infrastructure, connectivity and data feeds, surveillance systems. For venues handling 0.5% market share, these fixed costs represent operational drag before any profit margin.

As transparency platforms like FSB democratize venue measurement, institutional routers will increasingly concentrate flow toward Tier 1-2 venues with empirically validated differentiation. The fragmentation that Mehmet Kinak described—proliferation without innovation from 2005-2020—is reversing. Natural selection accelerates when measurement enables comparison.

The Bilateral Evolution

Mehmet Kinak describes a broader market shift:

"You're going to see more usage of direct bilateral engagement. It gives you the benefit of knowing who the other side is. If they know it's me, maybe they'll give me bigger size because they know I'm not going to run them over. To me, it's a better experience."

This bilateral evolution doesn't diminish the importance of the institutional ATS segment—it reinforces the transparency imperative. Whether liquidity flows through registered ATSs, hosted rooms, or direct bilateral arrangements, institutions need measurement frameworks proving which mechanisms preserve alpha.

Yet with 44.3 billion shares still executing through traditional ATSs monthly, transparency infrastructure remains the only path to comparable measurement. The venues succeeding long-term will be those offering bilateral-level explainability within ATS-scale liquidity aggregation.

VII. MARKET MAKER AND REGULATORY PERSPECTIVES

The liquidity provider and regulatory perspectives complete the market structure picture.

Market Maker Philosophy: Deterministic Access

A senior executive at a principal trading firm frames segmentation as the defining innovation of modern ATSs:

"The ATS world today is dominated by dark pools that have very sophisticated segmentation models. Scoring based on markouts and moving participants up or down the scorecard—giving them access to more or less segmented flow—that works pretty well."

Yet segmentation creates its own opacity, with logic varying dramatically across venues. The executive sees hosted rooms not as regulatory loophole but as logical evolution:

"Segmentation has gotten so sophisticated that hosted rooms and single-dealer platforms almost seem like the natural next step. The buy side sees the benefit of more direct interaction with liquidity providers."

The leader challenges the simplistic view that all market maker liquidity is predatory:

"The idea that all principal liquidity providers are toxic is wrong. We all have different characteristics, different time horizons, and different strengths. Bilateral relationships allow us to tailor those interactions—it's win-win."

"Bilateral trading lets you measure your counterparties directly. You can run A/B tests, assess fill quality, and tune your relationships. You can't do that in a mixed pool."

This emphasis on measurability aligns perfectly with FSB's value proposition and the broader transparency imperative.

Regulatory Recognition: Practical Modernization

A senior policy executive at a securities industry trade association summarizes the structural imbalance:

"There's a differential in the rule sets between the exchange and the ATS side. That allows people to innovate on the ATS side, whereas you can't really innovate on the exchange side—you have to do your rule filing, etc."

This structural asymmetry—ATSs innovate faster because they face fewer procedural barriers, while exchanges retain regulatory privileges that constrain experimentation—explains why venues like IntelligentCross, PureStream, and Blue Ocean operate under the ATS framework.

The executive connects exchange proliferation to regulatory incentives rather than innovation:

"You can make a good argument that all this fragmentation is due to the fact that you get free money just by opening an exchange. Right? Like the IEX—love it or hate it—was basically the last time we saw innovation in a new exchange."

On off-exchange growth:

"You see people flow to the off-exchange side because the ATSs are able to innovate more... but keep in mind the growth in retail. We've more than doubled retail participation, and that is all off-exchange."

This observation is critical: the 50% off-exchange share isn't solely regulatory arbitrage. The 74.5% of off-exchange that's retail wholesaling is driven by structural economics, while the 25.5% that's institutional ATSs is driven by matching innovation and execution quality differentiation.

The policy executive's reaction to the estimated 80 to 95% non-fill statistic demonstrates strong alignment with transparency initiatives:

“I didn’t realize when you said 90% of routes are unfilled. That’s fascinating to me. So you’re capturing the whole routing chain—each node? That’s powerful.”

This reaction underscores how both regulators and market participants increasingly recognize the oversight and commercial value of transparency infrastructure. As Jeffrey Estella, Principal at Estella LLC, notes:

“The Buyside needs to stick to their knitting of alpha generation and client relations. By leveraging partners who specialize in connectivity, unbiased data collection, non-attributed peer rankings, and venue routing based on meritocracy, asset managers can focus on what is key to them while gleaming actionable insights around their trading analytics.”

Together, these perspectives capture the convergence of regulatory oversight and buy-side innovation resulting in a unified vision where transparency is not simply compliance, but a competitive advantage shaping the next generation of market infrastructure.

VIII. THE PATH FORWARD: COORDINATED ACTION

Closing the transparency gap within the institutional ATS segment requires coordinated action across multiple fronts:

1. Measurement Infrastructure Aligned to Market Reality

Institutions need measurement frameworks reflecting how billions of shares executing through ATSs actually organize:

Tier 1/Tier 2 attribution given the 60/40 split

Institutional ATS isolation from retail flow

Venue-tier performance attribution across the four taxonomy levels

Market share contextualization for empirical evaluation

2. Broker Routing Transparency and Data Lineage

The 80 to 95% non-fill rate reveals a critical blindspot. Brokers must provide:

Complete routing analytics capturing all venue attempts, arrival timestamps, and rejection reasons

Venue-level attribution separating routing decisions from placement performance

Non-fill transparency distinguishing venues with poor efficiency from those with sophisticated adverse selection (trading against better-informed counterparties) protection

Standardized TCA frameworks enabling apples-to-apples venue comparison

Without granular routing data, even the most innovative venues remain unmeasurable to institutions. Broker disclosure transforms the institutional ATS ecosystem from opacity into measurability—unlocking the $11 billion in addressable execution improvements.

3. Infrastructure Diversity

The data center concentration problem—69% of ATSs operating from two adjacent facilities—requires active management. This concentration exists because rational economic incentives create systemic vulnerability. ATSs must position equidistant from NYSE and NASDAQ to avoid latency arbitrage when executing at NBBO midpoint.

Creating true resilience requires routing diversification, technology platform diversity, and clearing diversity. Encouraging innovation that shifts focus from price/time priority and latency competition toward execution quality metrics also helps address concentration challenges.

IX. CONCLUSION: WHEN TRANSPARENCY BEATS SPEED

Innovation in 2025 is no longer about who trades fastest, but it's about who can explain their trading.

Within the institutional ATS segment representing significant market volume, a smaller cohort of innovators is proving that transparency and structural differentiation can coexist with profitability:

MEMX enables venue innovation without capital-intensive buildout

Blue Ocean expands the market clock, trading 5,000 symbols nightly with displayed order book transparency

IntelligentCross enforces fairness through ML-driven determinism, achieving 16.1% market leadership

PureStream quantifies probability through volume-based matching

AlphaX US validates that batch auctions achieve institutional adoption through fast execution and bilateral price improvement

Fidelity Service Bureau provides the technology platform ensuring all of it is measurable

The Coming Consolidation

The data reveals an inevitable trajectory: the institutional ATS landscape will consolidate significantly over the next 3-5 years.

Economic pressure on Tier 3-4 venues is intensifying. Operating an ATS requires fixed costs that venues handling 1-2% market share cannot justify. The chart demonstrates this starkly: the bottom 20 venues collectively handle less than what IntelligentCross executes alone. When transparency infrastructure enables institutions to measure execution quality empirically, flow will concentrate toward venues demonstrating genuine differentiation.

Broker-run ATSs functioning primarily as internalization facilities face particular pressure. These venues often exist because they're operationally convenient for broker-dealers providing another destination for internal client crossing. But they impose costs on the broader ecosystem: routing complexity, measurement overhead, operational monitoring.

The market will consolidate around three distinct models: